The Transparency Trap: Learning from China’s ESG Disclosure Journey

ESG disclosure is now a must, but is it just about ticking boxes? We use China’s market as an example to dive into the real-world headaches and hurdles that global firms can’t seem to avoid.

Global ESG governance is moving from just "agreeing on ideas" to "following mandatory rules." Nowadays, disclosing ESG information has become the foundation for evaluating a company's long-term value and its ability to grow steadily.

Against this background, this paper goes beyond looking at just one single market. First, it describes the similarities and differences in how major economies build their ESG rules and supervision systems. Then, focusing on the Chinese A-share market, the paper analyses in depth the common challenges companies face during the first year of mandatory disclosure. Finally, it uses these findings to examine current developments and future trends in ESG disclosure in the global capital market.

Differences in ESG Disclosure and Practices Among Major Economies

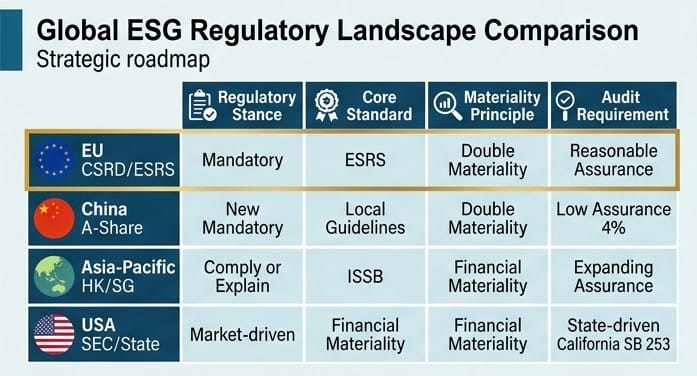

Despite different regional policies, China and the EU are showing a strong "regulatory harmony." Both sides have turned the principle of "Double Materiality" into legal duties, thereby redefining companies' social responsibility.

On September 12, 2025, China's Ministry of Finance released the "Basic Rules for Corporate Sustainability Disclosure (Trial)." These rules establish the general framework for China's ESG system, including basic standards, specific rules, and application guidelines. It serves as a practical guide for Chinese companies to follow the "double materiality" principle. It also provides clear instructions on complex topics such as value chain definition and risk analysis.

At the same time, the Shanghai, Shenzhen, and Beijing stock exchanges released their own reporting guidelines. This marks the end of "voluntary reporting" in China. Starting from 2026 (the first year of mandatory disclosure), ESG reporting will be a formal requirement, helping guide capital into green and sustainable areas.

The EU, known for the strictest ESG rules, built its system through the CSRD and ESRS. These rules require companies to combine sustainability information with financial data, linking ESG issues directly to core business performance. By requiring a specific electronic format (ESEF/XHTML), the EU is making sustainability data as easy to access and compare as financial data.

The ESRS standards, created by EFRAG, cover three main areas: First, Climate change, pollution, water, and circular economy; Second, A company’s own workers, people in the value chain, and consumers; Third, Business conduct.

This system requires companies to report not only how ESG issues affect their finances (Financial Materiality) but also how their business affects the world (Impact Materiality). It also requires third-party checks to ensure the information is reliable. In 2025, the EU and international organisations worked together to harmonise these rules, reducing the burden on companies required to comply with multiple standards.

In 2025, the EU adjusted its rules to help companies. On February 26, 2025, the EU proposed the "Omnibus Act" to update several laws. To give companies more time, they signed a "Stop-the-Clock Directive" in April 2025, delaying reporting for some smaller companies until 2028. The goal is to reduce pressure on businesses, especially small ones, while still maintaining overall green goals.

Based on this, EFRAG submitted a simplified version of the rules in December 2025. The final "Omnibus Act" was published in February 2026 and will take effect on March 18, 2026.

In the global ESG map, China and the EU are now working in sync. Both agree that financial numbers and social impact are equally important. China is entering a new era of mandatory disclosure with its new rules and stock exchange guidelines. Meanwhile, the EU continues to lead with its strict standards, especially regarding supply chains. This global trend shows that ESG is no longer just an "extra credit" task for companies; it has become a "must-have" for their daily operations.

Asia-Pacific and UK-Australia-New Zealand under the ISSB Framework

To stay competitive in the global market, major financial centres in the Asia-Pacific are quickly bringing ISSB standards into their local rules. Hong Kong and Singapore are leading the way, trying to keep international investors interested by Japan (SSBJ) and South Korea (KSSB) are following global standards while also focusing on their own local needs, especially in areas such as workplace diversity and transparency. Japan’s SSBJ rules, released in March 2025, are a milestone. Besides environmental rules, they emphasise the "Social" (S) part by requiring companies to disclose the gender pay gap and the ratio of female managers. Similarly, South Korea’s KSDS rules focus on "Climate First," requiring companies to identify climate risks. Before mandatory reporting starts in 2026, Korea already requires large companies to submit governance reports to build a solid foundation.

In contrast, the UK, Australia, and New Zealand are turning ESG disclosure into a legal duty through strict laws.

• The UK is merging several old rules into the UK SRS, focusing on financial risks (S1) and four main pillars of climate risk (S2): governance, strategy, risk management, and targets.

• Australia set up the ASRS framework, which is very similar to IFRS. It requires companies to report climate factors that affect their cash flow. Also, the Modern Slavery Act requires companies with over $100 million in revenue to check their supply chains, setting a high global standard for the "Social" dimension.

• New Zealand was the first country to make climate disclosure a law. However, its new government has recently shifted focus from "stopping climate change" to "adapting to climate change" due to budget cuts. This case shows how ESG rules can change when the economy or government changes.

Meanwhile, the US market looks very different. ESG policy has become a "political fight" between different states, and there is no unified national framework.

At the national level, the SEC tried to push for a unified climate disclosure rule in March 2024. New rules for climate info, based on IFRS S2, began on January 1, 2025. There are some "buffer" periods to make sure companies can follow the new rules without too much pressure. Meanwhile, Singapore is moving fast too. SGX RegCo announced that by 2025, all listed companies must report Scope 1 and Scope 2 emissions. Large ones will have to report Scope 3 starting in 2026. This shows that supervision is becoming much stricter, covering the entire supply chain now.

However, the real conflict in the US is between the "Red" and "Blue" states. Some Red states (like Texas and Florida) have passed "Anti-ESG" laws to stop companies from using ESG factors in business decisions. On the other hand, Blue states (led by California) are very aggressive. California passed laws requiring large companies to report all their carbon emissions (Scope 1, 2, and 3). While some of these laws are still facing court battles, California is still pushing forward with its strict climate reporting plans.

aligning their ESG rules with global standards. In September 2024, the Hong Kong Stock Exchange renamed its rules to the "ESG Reporting Code." Based on IFRS S2, these new climate disclosure rules took effect at the start of 2025. The policy provides a transition period so companies won't feel too much pressure. Singapore is also moving fast. Its regulator, SGX RegCo, told companies to report Scope 1 and 2 emissions in 2025, with Scope 3 emissions becoming mandatory for large corporations in 2026. This really pushes the supervision from simple numbers to the whole business process.

In the global ESG field, major markets have developed very different systems and paths. By using "Double Materiality" and CSRD, the EU now has the most complete rules in the world, requiring both reporting and audits. But the US is different—its national rules aren't very stable and mostly care about financial data, though laws in certain states are making progress. At the same time, the UK and Australia are prioritising climate info by adopting ISSB standards to keep up with global capital. In Asia, we see Japan and South Korea moving fast toward mandatory disclosure with a clear focus on how companies are managed. China’s disclosure is guided by national goals like "Carbon Neutrality," emphasising mandatory environmental information and policy consistency.

Although their rules differ, companies worldwide are facing the painful shift from "Public Relations" to "Data Management." We can see this struggle clearly in 2026, as it's the first time A-share companies in China have been forced to disclose ESG information. Today, ESG is not just about compliance. It is starting to reshape a company’s spending, its market price, and its ability to compete over many years.

To see how these rules work in real life, the second chapter of this paper will compare the performance of markets in China (A-shares), Hong Kong, the EU, the US, and Singapore during the 2025 reporting cycle. We will focus on: the coverage of GHG emissions (Scopes 1-3) and how well they align with international standards, and the "compliance gap" between leading large companies and small-to-medium ones. Our goal is to help market participants identify and address their key weaknesses as they move toward mandatory and international ESG reporting.

A Global View of ESG Disclosure in Capital Markets

As global markets change their expectations, China’s A-share market shows a clear "gap between quantity and quality." While leading companies have almost reached full coverage, the overall quality and reliability of reports across the market still need improvement.

The year 2025 is a milestone for China’s A-share ESG progress. With over 2,500 companies sharing their 2024 reports, the disclosure rate jumped to an all-time high of 46.8%. The biggest players—those worth over 100 billion yuan—are leading the way with a 99.27% reporting rate. This really shows that ESG has moved from an "extra" task to a basic requirement for any large corporation today.

In terms of industries, the financial sector continues to lead, while high-carbon industries such as steel and transportation are catching up quickly due to "Carbon Neutrality" policies. Our survey shows that 67.27% of companies have established dedicated ESG management teams, and 63.93% have shared their strategic information. Moreover, 78.07% conducted "materiality assessments" to identify their core issues, and 93.32% established communication channels with their stakeholders.

Regarding climate data—which the international market cares about most—there is still significant room for improvement. Although 62.07% of companies identified climate risks and opportunities, the data remains weak. Around 60% of companies Finally, we found that the Main Boards of the Shanghai and Shenzhen exchanges performed best in terms of participation and standards. In contrast, while the ChiNext market is trying hard to catch up, it still lags behind the leading companies in terms of report quality and third-party checks. This shows a typical early-stage feature: "top companies lead the way, while smaller ones are still waiting and watching."

At the same time, the Hong Kong market has built an ecosystem led by "top examples." While large companies in the HangSeng Index lead the world in adhering to international rules and receiving external checks, smaller companies are still at the stage of "just following basic rules."

The Hong Kong market has a very high baseline for compliance. Most companies have a disclosure rate of over 90% across 12 different environmental and social areas, with only "Labour Standards" being slightly lower at around 80%. On the climate side, nearly 97% of companies report Scope 1 and 2 emissions. Even Scope 3 reporting has grown steadily from 37% last year to 41%.

The leading effect of large-cap companies is becoming more obvious. Taking the HangSeng Composite LargeCap Index as an example, 100% of these companies now cover Scope 1 and 2. Their Scope 3 disclosure rate also jumped from 50% to 69%, with a focus on high-value areas, including purchasing (76%), business travel (79%), and employee commuting (60%). Additionally, many of these big players refer to international standards: about 70% use GRI, 64% use TCFD, and 47% use ISSB. Overall, these large companies are leading the change from "quantity to quality." They are well-prepared for the upcoming mandatory climate rules. However, they still need to improve the transparency and comparability of their Scope 3 data across different firms.

In contrast, smaller companies and those on the GEM board are falling behind. Most businesses that fail to report Scope 3 are small or medium-sized. For these companies, ESG reporting is still mainly about meeting the minimum legal requirements. They rarely use international frameworks, conduct climate analyses, or hire third parties to verify their data. Their reports usually stick to basic numbers or simple descriptions, and they rarely link ESG info to their business strategies or financial performance.

By comparison, the EU has set a "high standard" for global regulation by showing a very high level of Scope 3 reporting (87%). Under the mandatory CSRD and ESRS rules, about 92% of listed companies in the EU disclosed their Scope 1 and 2 emissions. More importantly, the Scope 3 rate reached 87%, indicating that EU companies are actively organising their supply chain data. This performance is truly outstanding in the global market.

By emphasising clear numbers, risk analysis, and standardised formats—while also staying consistent with international standards such as TCFD and GRI—the EU ensures its data quality and comparability are much better than in voluntary markets. However, reporting Scope 3 in full detail remains a "bottleneck" even for the EU, especially for medium-sized companies and their supply chains. This is quite similar to the global trend.

On the policy side, the EU's CSRD and ESRS are among the most organised and strict ESG frameworks globally. They don't just tell companies what to report, but also focus on specific data, risk links, and standard structures. This makes the data from EU companies easier to compare and more reliable than in markets where reporting is voluntary. Meanwhile, although the ESRS is an "internal EU standard," it is compatible with international frameworks, which further helps global investors easily compare the data.

In 2025, ESG disclosure in the US stock market is still mostly voluntary. However, among large listed companies, the coverage is extremely high. For example, nearly 99% of S&P 500 companies and about 94% of Russell 1000 companies have released sustainability reports. This shows that ESG reporting has become a mainstream practice. Reporting on Scope 1 and Scope 2 emissions is now common, and even Scope 3 reporting is very popular among large firms (nearly 99% of S&P companies cover it). Even without a unified national law, investor and market demands are pushing companies to adopt international standards. At the same time, although the language used in these reports is changing due to the political environment, the overall focus on climate risks and sustainability remains very strong. Even amid uncertainty at the federal level, state laws and international trends continue to push US companies toward greater transparency.

Besides these major markets, it’s worth noting that Singapore’s stock market entered a mature, organised stage for ESG disclosure in 2025. Among all SGX-listed companies, 529 have already published sustainability or ESG reports, showing a high coverage rate. About 97% of these companies include at least one piece of climate-related information in their reports, and many follow many of the TCFD recommendations. This shows that Singaporean companies care deeply about climate issues. Regarding greenhouse gas emissions, reporting on energy-related data is quite mature: about 80% of companies disclosed Scope 1 data, and about 87% disclosed Scope 2. In contrast, the Scope 3 rate is much lower, at about 29%.

reported Scope 1 and 2 emissions, but only 11.37% reported Scope 3 emissions, which measure the broader supply chain. Also, only 24.87% set clear emission-reduction targets, and very few (around 16-17%) provided a clear timeline for reaching "Carbon Peak" or "Carbon Neutrality."

Regarding international standards, 97% of companies have followed TCFD suggestions to some extent. However, only about 32% of them covered all 11 recommended items. This shows that most companies are still picking and choosing parts of international rules rather than following them completely. Overall, the Singapore market is well ahead of the global average in terms of "how many" companies report. But in terms of "how deep" they go—especially with Scope 3 and strict international rules—they are still in a transition stage from voluntary to high-standard reporting.

The differences in rules and maturity across major markets are now reshaping companies' global competitiveness. Looking around the world, ESG reporting has shifted from "simple reporting" to "strategic matching." This evolution reveals three main trends:

First, emerging markets like China’s A-share market have finished their initial jump in coverage. Now, they are at a turning point, moving from "quantity" to "quality." The key to breaking through their management bottleneck is to fill the Scope 3 data gap and link their data to core business strategies. Second, the EU’s strict rules have set a "high standard" for the world. This means that data without independent audits or supply chain support will slowly lose its credibility. This is exactly the challenge that small and medium-sized companies in Hong Kong need to overcome. Third, the experience of large companies in the US, Singapore, and Hong Kong shows that adopting international standards like the ISSB early is a smart strategy. It helps them lower communication costs in complex supply chains and secure cheaper financing.

This global upgrade of rules and standards has created a common language, but it also brings "growing pains" for companies at different stages. We must realise that the challenges faced by Chinese A-share companies in their first year of mandatory disclosure are not unique. Instead, they are a perfect example of how global ESG governance is evolving. Whether it is missing data or a gap in strategy, these issues reflect the global shift from "PR-driven" to "value-driven." Next, we will look closer at these examples to uncover the "brand-style" mistakes hidden behind high disclosure rates. By analysing problems such as poor data comparability and hidden penalty information, we hope to provide a warning and a guide for corporate ESG management in the global green economy.

Looking at the A-share Sample: Uncovering ESG Mistakes of Global Companies

In 2026, China’s A-share market faced its first "big exam" for mandatory ESG disclosure. The stock exchanges in Shanghai, Shenzhen, and Beijing set a deadline of April 30, 2026, for 470 major companies to finish their first ESG reports. Since these new rules were introduced in April 2024, the number of A-share companies sharing ESG data has jumped significantly, reaching 47%. By the middle of April 2026, close to 1,000 companies had already prepared their reports. This clearly shows that the whole process is on the right track and moving forward quite smoothly.

However, this "successful" image hides some serious gaps. Many reports are missing key data or only share the good news, and outsiders haven't checked most of them. It’s a shame that some firms treat ESG reports as just another ad for their brand. This is a classic mistake worldwide—companies find it hard to stop "storytelling" and start doing real management. This is a common trap for firms globally as they struggle to move from just "telling a good story" to actually managing their impact.

Faced with the pressure of following rules while lacking the ability to manage data, many companies are choosing a "strategic" way out. Specifically, many reports use simple descriptions to hide the "missing numbers." Although the new guidelines require more quantitative data, calculating key metrics—such as Scope 3—can be very costly. As a result, many firms choose to use vague words to avoid meeting the actual calculation standards.

The guidelines from the three stock exchanges have set clear standards for 21 core issues, such as waste emissions and the use of energy and water. However, many reports still use simple "word descriptions" to hide the "missing numbers."

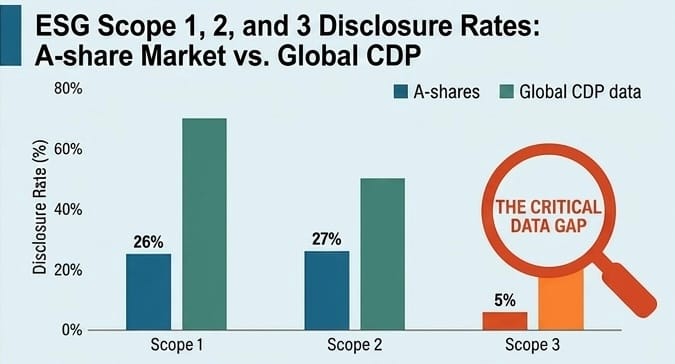

Take greenhouse gas emissions as an example. According to the Sino-Securities Index, the reporting rates for Scope 1 and Scope 2 among A-share companies in 2024 were surprisingly low—only about 26% and 27%. For Scope 3, which is much harder to track, the number dropped to a tiny 5%. Compared to global figures from CDP, where the rates hit 70%, 50%, and 20%, it’s clear that Chinese companies still have a long way to go. The difference is really huge. On top of that, nearly 10% of companies are still using the old name "Social Responsibility Report." Their content focuses more on charity and donations, which is quite different from the standard ESG framework.

Scope 3 carbon emissions are currently a hot topic in the international ESG field, but the high cost of collecting data is a major reason why disclosure rates remain low. Reporting Scope 1 and 2 is relatively easy because it only involves a company’s own data. However, Scope 3 covers 15 complex categories. The data comes from many sources and requires extensive communication between subsidiaries and partners. It is also necessary to verify that the data is real and accurate, which makes the process extremely time-consuming. For most companies, collecting and processing ESG data, especially environmental data, is a huge task. Since many firms struggle to meet official standards, they often use vague descriptions to avoid doing the actual math.

For example, China Satellite did not share any carbon emission data in its ESG report. In the "Metrics and Targets" section of the climate chapter, they stated that the company "continues to push all units to save energy and reduce carbon by improving management and using new technologies." However, they didn't provide a single number for their carbon emissions. This kind of reporting, which lacks clear targets and baseline data, is very common in the global market. In fact, it is basically "disclosure without a baseline."

However, even if companies move past the first step of "having data," people still doubt whether the reports can be compared. This is mainly because of the "maze" effect caused by different calculation methods. Because companies don't use the same math, even two firms with similar sizes and businesses might show very different results for carbon emissions. When you add the problem of following rules across different countries, the data becomes even harder to compare.

Even when numbers are provided, they aren't very useful if the calculation methods are inconsistent. For example, some listed companies look very similar on the outside, but their carbon emission data is surprisingly different. The root cause is simply that they don't count the same things in the same way. Although the guidelines released in January 2026 provided a detailed framework and mathematical formulas for climate and energy issues, ensuring everyone produces standardised data remains a huge challenge.

Another difficulty is the difference between industries and company sizes. "Heavy" industries that use a lot of energy care about very different things compared to "asset-light" companies (like tech or services). Also, small and medium-sized companies aren't as good at managing data as big corporations. If the government forces them to maintain the same high standards, it might lead to "inaccurate data" or even greater risks, such as data cheating and "greenwashing."

Finally, companies doing business overseas must balance domestic and foreign rules. This pressure for "cross-border compliance" is becoming a global headache, making it even harder to compare ESG data across companies in different regions.

Differences in calculation methods might stem from a lack of technical skills, but choosing what information to share is a matter of honesty. Too many companies are choosing to keep their bad news secret, turning the whole thing into a "trust game" between firms and investors. By only sharing the good stuff, they’ve basically turned ESG reports into fancy brand booklets. This means serious risks,like environmental fines or workplace accidents,are hidden in a "blind spot."

The official guidelines clearly state that listed companies must disclose penalties related to the environment, safety, quality, and unfair competition. They need to report the reasons for the penalty, the amount fined, how it affects the business, and what they are doing to fix it. Companies are not allowed to pick and choose what they share. They are also required to follow the "Double Materiality" principle,considering both financial impact and social impact,when deciding what is important. However, many firms still treat ESG reports as marketing booklets and avoid mentioning any "red line" info.

Take Datang Power as an example: one of its subsidiaries was caught illegally using grassland for coal waste in 2025. In addition, Shanghai Construction Group was forced to pay 1.8 million yuan for illegal nighttime work and for failing to report its waste plans. Even though these were big stories, both companies completely left them out of their ESG reports.

Similarly, Nanjing Panda received a warning for inaccurate financial forecasts, and Kinglong Holdings was ordered to address issues related to fake trade deals. Usually, information about penalties in corporate governance is more public. But even if these details were already mentioned in annual financial reports, many companies still choose to ignore them in their ESG reports. This "disconnect" between financial data and ESG info seriously damages the credibility of non-financial reporting.

If companies can hide penalties that are already on public record, then the risks in supply chains, overseas projects, and partner companies are even more likely to stay in the "blind spot" of ESG reporting. Companies often weigh the costs and benefits of disclosure. They carefully decide whether to report and how much to share; if the data looks bad, they choose not to disclose it. Furthermore, ESG data is scattered across different departments. Many department heads worry that negative news will damage their reputations, so they are unwilling to provide complete data. Without any positive rewards for high-quality reporting, it is very hard for companies to achieve full transparency.

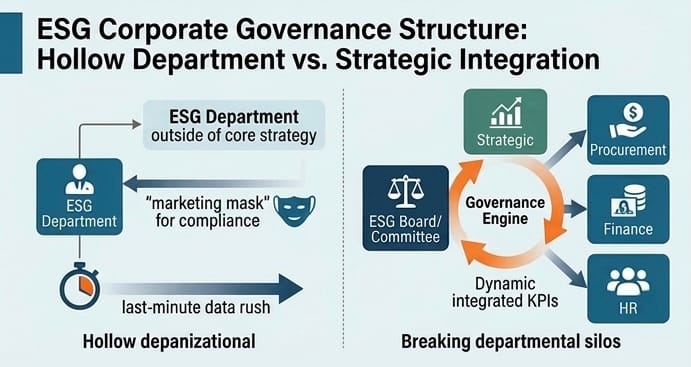

The root cause of this disconnect between reporting and real risk is often a "mismatch" in the company’s internal management structure. In the A-share market, it has become common for ESG committees to become "empty departments." Because the organisation is hollow, ESG decisions are rarely integrated into the company’s core strategy. As a result, ESG work often becomes a mere formality—a "marketing mask" created to satisfy regulators.

Currently, nearly 1,000 A-share companies have set up ESG committees. While these committees are technically responsible for ESG strategies and targets, they often don’t do much in practice. It’s a classic case of a "hollow" department. Because of this, ESG has become just a second face for branding, rather than a real force that changes the company’s core management.

Many corporate ESG committees have unclear responsibilities and lack transparency. Because they don't have a regular management system, data is often rushed together just before the deadline. This makes people doubt whether the data is accurate or consistent. Furthermore, many companies still wonder about the actual value of ESG. They don't understand why they need to report certain metrics and see it as a legal burden. To prevent the ESG department from becoming useless, companies must set up clear daily work routines and link ESG performance to employee rewards. Otherwise, they will easily fall into the trap of "reporting just for the sake of reporting."

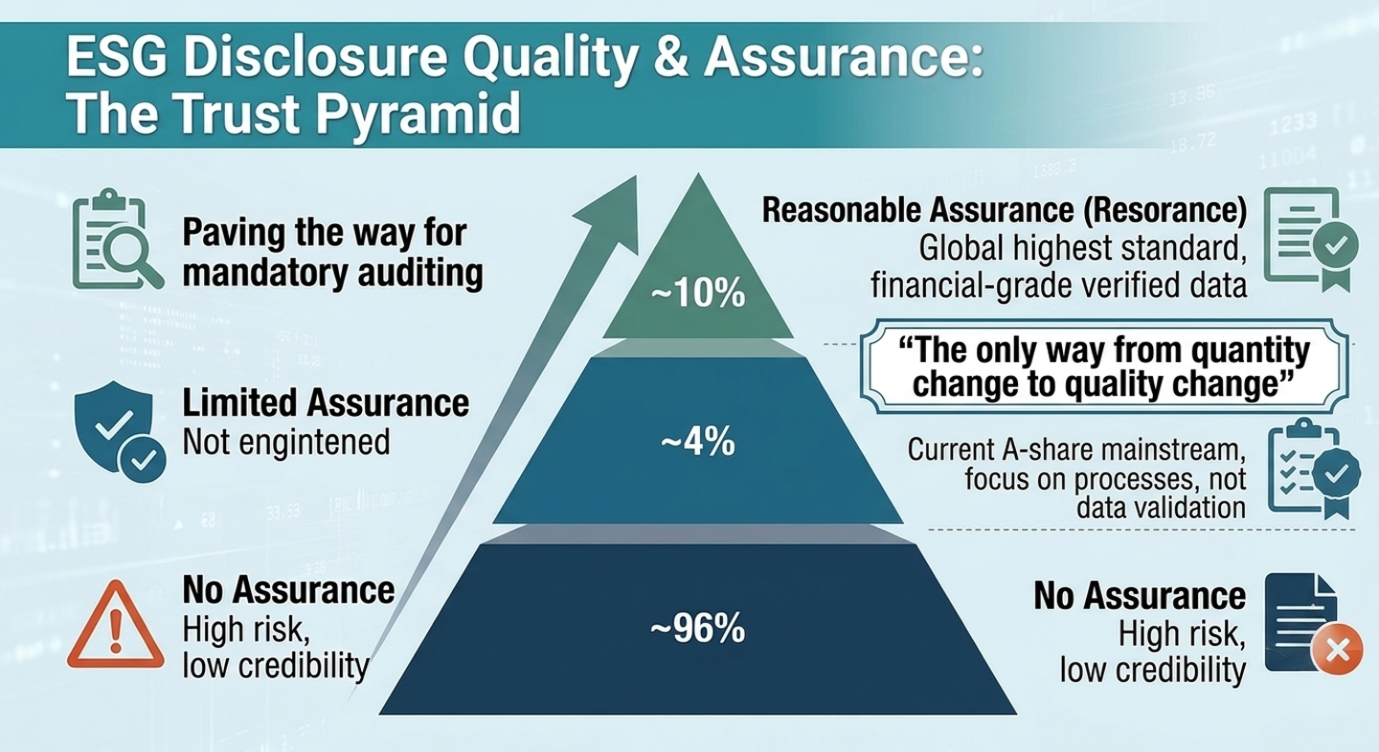

When internal management fails, external audits should act as the "last line of defence." However, in reality, price wars and low-cost competition have led to a lack of quality checks, leaving data without any real protection. Currently, the rate of third-party assurance in the A-share market is extremely low. Most of these checks remain at the "limited assurance" level, which provides very little coverage. This weak supervision makes it easier for companies to hide bad news or engage in "greenwashing."

At the beginning of 2026, the Ministry of Finance released basic standards for ESG assurance to organise the process. However, data from the Sino-Securities Index shows that only 200 A-share companies had their 2024 ESG reports checked by external parties. The external assurance rate is currently only about 4%. Even leading companies like Hengrui Medicine and Great Wall Motor, which are required to report, did not hire third-party agencies for these checks. Currently, most of these services are provided by accounting firms and a few other qualified organisations.

Currently, third-party ESG assurance faces several major challenges. First, the standards are fragmented as different agencies use very different methods and metrics, leading to inconsistent quality. Second, agencies cannot identify risks; they are not very good at spotting "greenwashing," "bluewashing," or selective reporting. Third, the industry still lacks a strong mechanism for quality control.

Most current checks are only "limited assurance" and cover very little (sometimes as little as 1% of the report). The risk associated with "limited assurance" is much higher than that with "reasonable assurance." Right now, most A-share ESG checks focus on reviewing processes and risks rather than verifying data accuracy. The root cause is that many companies hide too much information and are afraid to accept the higher-level "reasonable assurance" check.

These mistakes in China’s A-share market are a "painful but necessary stage" for companies globally during the early days of mandatory ESG rules. It reminds us that high-quality ESG reporting cannot rely solely on rules. It requires a real change in a company’s internal management. Only by breaking the habit of "marketing-style reporting" and returning to data honesty can companies turn ESG into a long-term competitive advantage and a solid base for their market value. As we have seen in pioneering markets like New Zealand, these growing pains are unavoidable, but the only way to long-term success.

Conclusion

Looking at the world today, the era of "picking what to tell" in ESG reporting is over. We have officially entered a new stage of "mandatory and standard rules," driven by frameworks such as the ISSB and CSRD. From the EU setting the world’s strictest auditing standards, to financial hubs like Hong Kong and Singapore quickly following global rules, and countries like the UK, Australia, and New Zealand making climate reports a legal duty—everyone is moving. Although each market has its own pace and philosophy, one thing is now clear: how transparent and detailed a company's data is will directly decide where global capital flows.

By looking closely at China’s A-share market as a key example of this change, we can see that "high reporting numbers" do not always mean "high-quality management." Taking its first "big exam," the A-share market struggled with several key issues. The data was far from complete—Scope 3, for instance, was only 5%—and inconsistent math made it hard to trust the results. On top of that, many ESG departments felt hollow. These struggles aren't unique to China; they are common growing pains for any firm globally trying to get serious about following the rules.

These mistakes serve as a strong warning: an ESG report should not be a "PR brochure" used to make a company look good. Instead, it should be a "microscope" that truly analyses a company’s strengths and its potential for long-term growth.

In 2026, to stay competitive in the global green economy, we must move beyond mere formalities and focus on the core. This requires a big change in three areas:

First, we must stop the "last-minute data rush" just before the reporting deadline. Companies need to break down departmental walls and build a robust system for collecting Scope 3 data across the entire supply chain. Only by integrating ESG data into daily management can we truly embed sustainability at the heart of a business.

Second, companies should stop seeing disclosure as just a cost. Instead, they should use it as a strategic tool to improve their capital structure, lower their financing costs, and attract long-term investors. By being transparent, companies can secure a "valuation premium"—making their business more valuable in the eyes of the market.

Third, the ESG committee must do real work, not just exist on paper. Companies should avoid a "hollow" structure and lead the way in hiring high-standard third parties to review their reports. Using real and verified data is the only way to beat "greenwashing" claims and build solid trust with the market.

The evolution of ESG standards is, at its heart, a deep reshaping of global business culture. Early markets like New Zealand show us that the green trend is unstoppable, regardless of small policy shifts during economic cycles. The "pain" we see in China’s A-share market is really just a learning process for global ESG. From here on out, only companies that stop hiding behind PR and start facing their data gaps head-on will come out on top. That’s how they’ll turn ESG from a compliance burden into a real source of long-term strength.

References

- ISSB (International Sustainability Standards Board). (2023). IFRS S1 & S2: Sustainability and Climate-related Disclosures.

- IFRS Foundation & EFRAG. (2024). Interoperability Guidance on ISSB Standards and ESRS.

- CDP (Carbon Disclosure Project). (2024). Global Corporate Climate Change Disclosure Report.

- Ministry of Finance of the People's Republic of China. (2025). Sustainability Disclosure Standards for Enterprises — Basic Standards (Trial).

- Shanghai, Shenzhen, and Beijing Stock Exchanges. (2024). Guidelines on Sustainability Reporting for Listed Companies (Trial).

- Sino-Securities Index (Huazheng Index). (2025). Analysis Report on ESG Disclosure Quality and Greenhouse Gas Data for A-share Listed Companies

- HKEX. (2024). Consultation Paper: Enhancement of Climate-related Disclosures.

- European Union. (2022). Corporate Sustainability Reporting Directive (CSRD).

- EFRAG. (2023). First Set of European Sustainability Reporting Standards (ESRS).

- European Commission. (2026). Omnibus Act: Streamlining Sustainability Reporting and EU Taxonomy.

- U.S. SEC. (2024). The Enhancement and Standardization of Climate-Related Disclosures for Investors.

- California State Legislature. (2024). SB 253: Climate Corporate Data Accountability Act.

- Financial Markets Authority (New Zealand). (2021). Climate-related Disclosures (CRD) Framework.

- Australian Government. (2024). Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Bill.

- SGX RegCo (Singapore). (2024). Roadmap for Mandatory Climate Reporting for Listed Issuers.