Global Corporate Social Responsibility Research: An In-Depth Analysis of the Current Global ESG Landscape

In March 2026, global environmental, social, and governance (ESG) issues were undergoing a profound test of "institutional maturity."

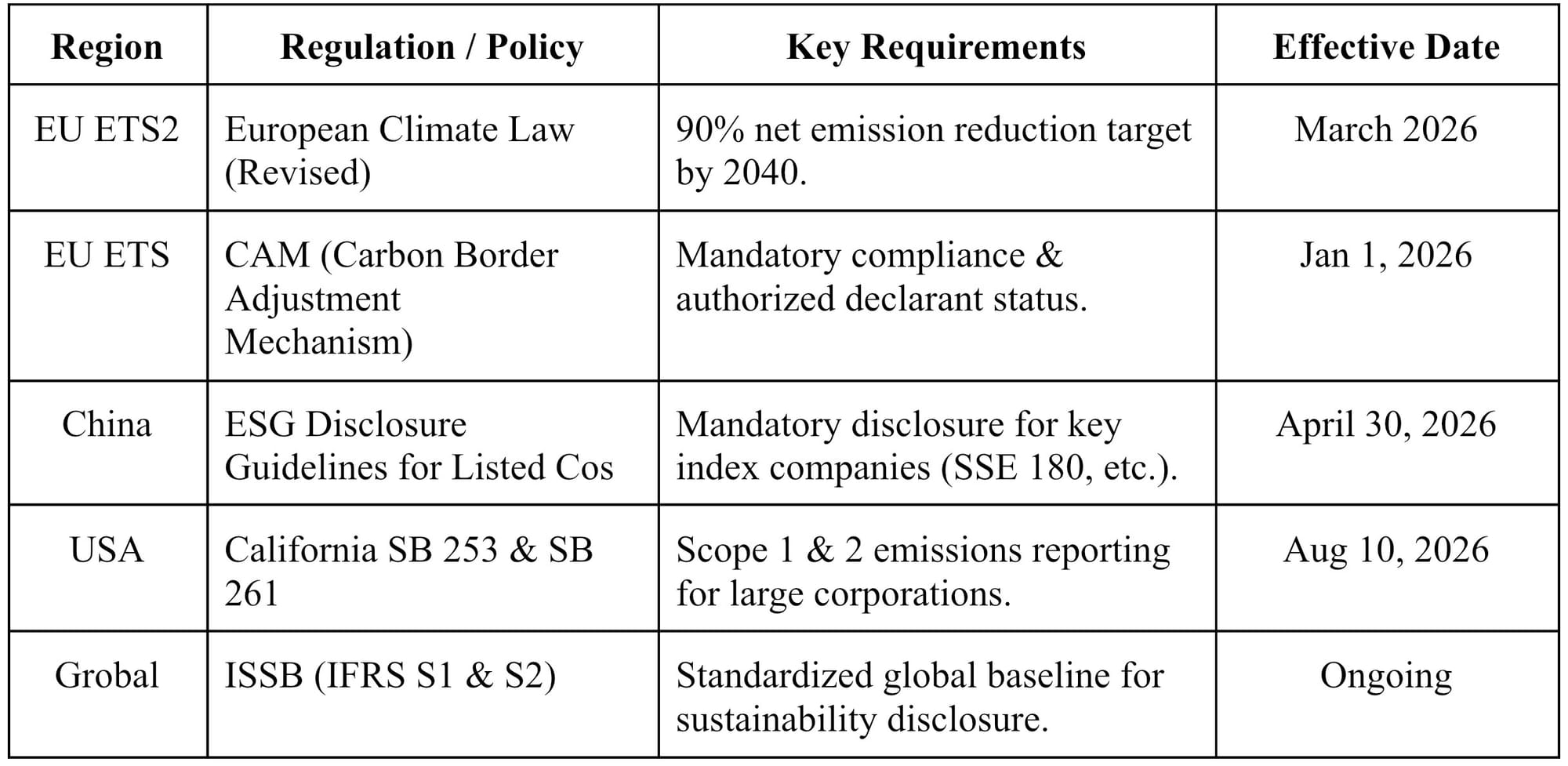

On one hand, major economies are continuously deepening the institutional supply in the field of climate regulation—the EU has established a 90% emission reduction target by 2040 through revisions to the European Climate Law and launched the world's first permanent carbon removal certification standard; China's A-share mandatory ESG disclosure "first test" has been fully launched; and carbon pricing and disclosure mechanisms in many countries have moved from policy declaration to substantive implementation.

On the other hand, tensions and frictions in institutional implementation have significantly intensified. The implementation of the CBAM has triggered a shockwave in trade compliance; the breakdown of COP30 negotiations has exposed the deep-seated failures of multilateral climate governance mechanisms; and Vanguard's massive settlement and Glencore's greenwashing lawsuit reveal the critical point for the transformation of ESG accountability mechanisms from "soft constraints" to "hard constraints."

Using current key global ESG events as a starting point to deeply analysis the structural tension between deepening regulation and resistance to implementation, explore its multidimensional impact on the global governance order, corporate strategy, and investment logic, and propose a practical response framework.

The Current Global ESG Landscape

In 2026, ten years will have passed since the Paris Agreement was adopted, more than four months since COP30 concluded in Belém, Brazil, just three months since the EU's Carbon Border Adjustment Mechanism (CBAM) officially came into effect, and only one month until the final deadline for mandatory ESG disclosure in China's A-share market. This convergence of events should have been a highlight, a turning point in global ESG governance from blueprint to reality. However, reality is far more complex than imagined.

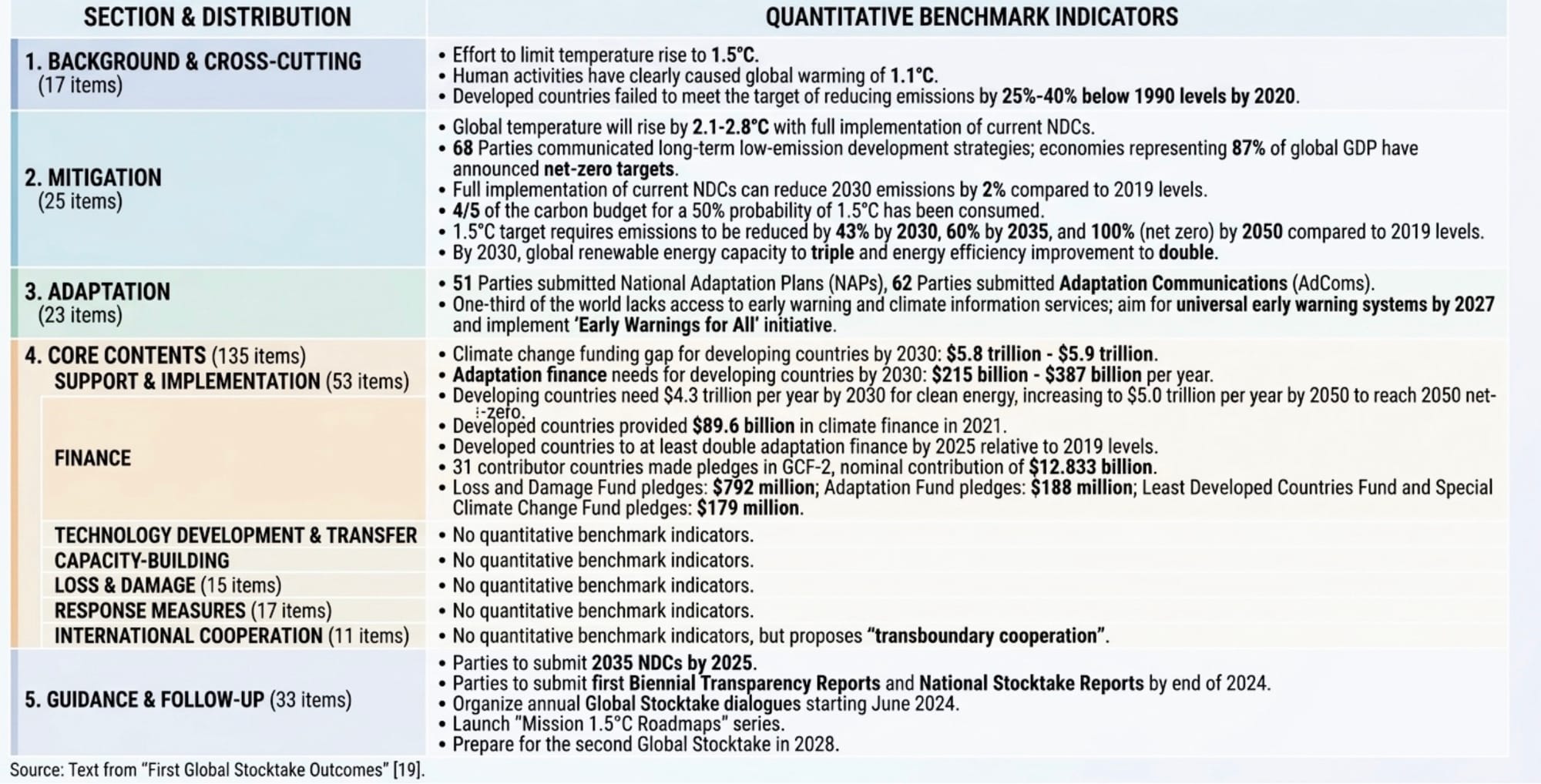

This complexity comes from the sharp mismatch highlighted by the First Global Stocktake (GST). On the one hand, the GST set clear numerical benchmarks—such as the need to triple global renewable energy capacity and double energy efficiency by 2030. On the other hand, it revealed an enormous “implementation gap.” To stay on track for the 1.5℃ goal, global emissions would have to be cut by 43% by 2030 and 60% by 2035 compared with 2019 levels; yet the current NDCs (National Determined Contributions) are only expected to achieve about a 2% reduction by the end of the decade. That shortfall is made even worse by a large “finance deficit,” since the $5.8–$5.9 trillion needed to support developing countries sharply contrasts with the climate finance actually being mobilised by developed nations, which has been meagre and underwhelming. As a result, the GST is more than just a report card. It is essentially a mathematical demonstration of the structural conflict between ambitious global goals and the slow, limited reality of national delivery.

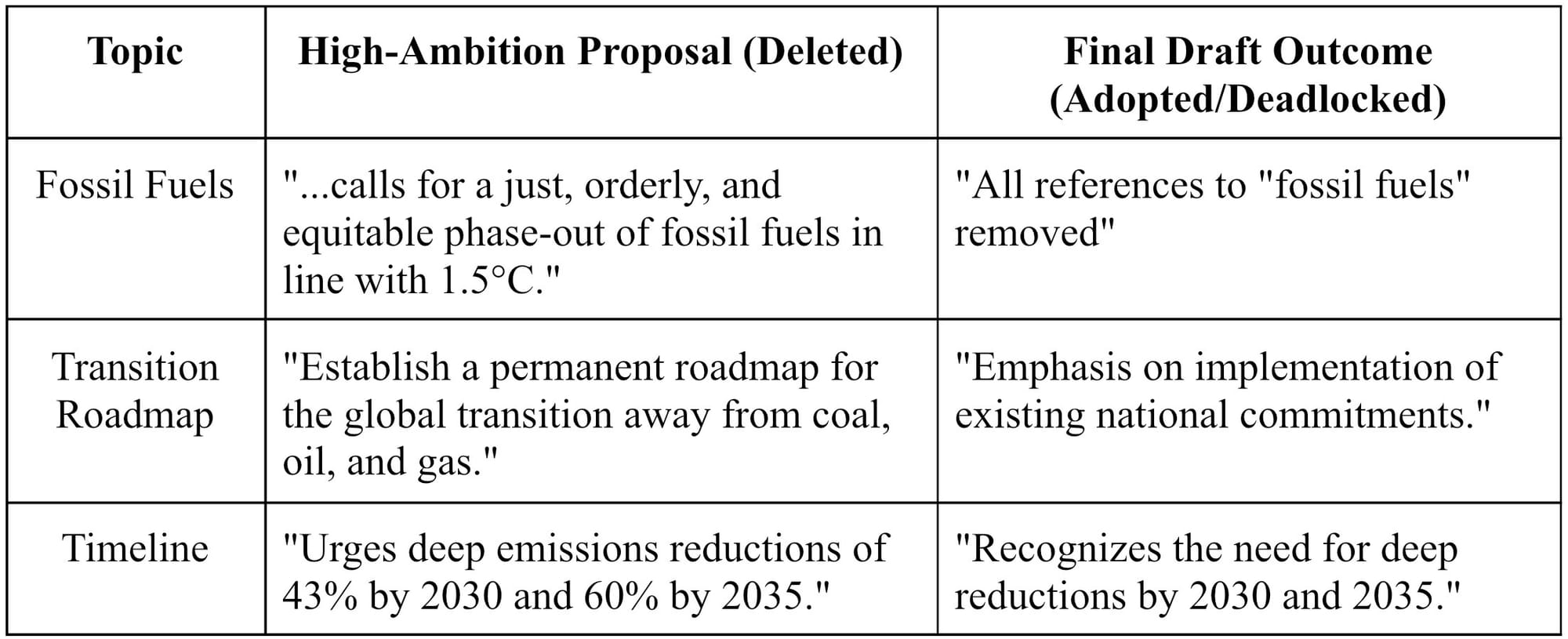

In March of this year, the COP30 negotiations in Belém ended in a dramatic stalemate—the host country, Brazil, removed all references to "fossil fuels" and "transition roadmaps" from its draft text, the EU warned of a "possible no-deal ending," and more than 80 countries left disappointed. This setback is not an isolated case. In additional, the European Council adopted the revised European Climate Law, incorporating a 90% emissions reduction target by 2040 into a legally binding medium-term goal; China's three major stock exchanges revised and released their ESG reporting guidelines, marking a new stage in the refinement of their information disclosure systems; the China Council for the Promotion of International Trade (CCPIT) officially entered a mandatory compliance period, with the March 31st deadline for authorized reporting entities becoming a Damocles' sword hanging over global exporters. SEC’s climate rules remain on hold amid ongoing legal drama. Meanwhile, Vanguard just dropped nearly $30 million to settle a lawsuit tied to its ESG moves — it's basically retreatin

Deepening Management: Three Dimensions of Current ESG Institutional Supply

Climate Ambitions: An Institutional Leap from Commitment to Legislation

On March 5, 2026, the Council of the European Union formally adopted the revised European Climate Law, setting a legally binding medium-term climate target for 2040—that the EU's net greenhouse gas emissions must be reduced by 90% from 1990 levels by 2040. The main point of this reform is to establish transparency at the transition point between 2030 and 2050. According to the communiqué, 85% of emissions must be reduced by 1990 in the EU, while the remaining 5 percentage points must be reduced from 2036 onwards through “high-quality international carbon credits” from other countries.These carbon credits must come from "credible greenhouse gas emission reduction activities of partner countries" and comply with the Paris Agreement.

from trying to push companies to change through its shares. And Glencore is getting heat; it is being sued by organisations in Australia for ‘greenwashing’ and misrepresenting its environmental harm.

If you're wondering what the hell is going on with ESG, all of that might seem random, but it’s actually symptomatic of what’s Actually Happening With ESG Right Now. In effect, while all this rulemaking continues and intensifies, enforcement is becoming much more difficult. There’s this giant wave of new regulations coming at full steam, and at the same time, the pushback and drama surrounding them is rivalling them. I believe that understanding this structural tension between "deepening regulations and calibrating enforcement" is key to grasping current and future ESG development trends.

The profound impact of this law lies in three levels. First, the bill formally recognises permanent carbon removal technology for the first time, sending a clear signal of a technological roadmap—the EU has implicitly acknowledged that deep decarbonization in some industries must rely on engineering methods, rather than solely on energy substitution. Second, a bill allows international carbon credits, but only 5% of global carbon credits can be used, so companies cannot simply use foreign offsets or avoid carbon production altogether. Third, this move will force emerging market countries to accelerate the development of high-standard carbon credit certification systems, as substandard carbon credits will be barred from entering the EU market.

Almost simultaneously, on February 3rd, the EU officially adopted the world's first permanent carbon removal certification standard. This standard aims to transform carbon removal into "financial-grade" assets by imposing stringent legal constraints, thereby ending the chaotic "green drift" in the voluntary carbon market. These two pieces of legislation—the 2040 climate target and the carbon removal certification standard—constitute a closed-loop system for EU climate governance, extending from "mitigation" to "removal," marking a new stage in global carbon governance: engineering-based decarbonization.

Meanwhile, in China, the 2026 government work report has just been issued. They have secured a target to reduce carbon intensity by close to 3.8%. Now that they've made it a 'quantitative binding target,' it's a mandatory goal they must meet by the end of the year. This goal comprehensively considers various needs, including economic and social development, green and low-carbon transformation, and national energy security. It is conducive to achieving the carbon peak target in an orderly manner before 2030. With the inclusion of industries such as steel and non-ferrous metals in the national carbon market, the carbon price discovery mechanism will be further improved, and carbon emission data accounting, verification, and carbon footprint management will become core compliance work for enterprises.

The Disclosure Revolution: From Voluntary to Mandatory Institutional Transformation

2026 marks the first year of rigorous ESG information disclosure for A-share listed companies. According to the "Guidelines for Sustainable Development Reports of Listed Companies" issued by the three major stock exchanges, companies included in the SSE 180, STAR Market 50, SZSE 100, and ChiNext indices, as well as companies listed both domestically and overseas, are required to disclose their 2025 sustainable development reports for the first time by April 30, 2026. These guidelines establish a mandatory disclosure framework covering 21 topics across three dimensions: environment, society, and governance.

By March, the system's implementation accelerated. On January 30, the three major stock exchanges simultaneously revised and released the "Guidelines for the Preparation of Sustainable Development Reports of Listed Companies," adding three new application guidelines: "No. 3 Pollutant Emissions," "No. 4 Energy Utilisation," and "No. 5 Water Resource Utilisation." Both Chinese and English versions were simultaneously released to global investors. On March 27, the Shanghai Stock Exchange (SSE) further compiled and released the "Representative Case Studies of Sustainable Information Disclosure by Shanghai-listed Companies," which gathers 56 representative case studies from listed companies with high ESG ratings from the China Securities Regulatory Commission (CSRC), providing insightful and practical references for compiling high-quality ESG reports.

As of March 29, at least 257 A-share listed companies had disclosed their 2025 ESG reports, with the pharmaceutical, biotechnology, and electronics industries leading in the number of disclosures(For a detailed sectoral breakdown and index composition, please see Appendix C). Looking at the disclosed reports, data quality has become a crucial "scoring point" in this "first test"—more and more companies are beginning to disclose comparable data over several consecutive years, incorporating ESG performance into their senior management assessment systems, disclosing specific topics such as biodiversity and climate transition, and even disclosing third-party verification. The head of Sustainability and Climate Research for Greater China at MSCI noted that these policies are, in principle, consistent with the International Sustainability Standards Board (ISSB), and that global investors are strongly supportive of the introduction of relevant policies in the Chinese market.

Unlike China's institutional development, the US SEC climate disclosure rules are frozen at the judicial gate. The March 2024 rule mandates that publicly traded companies disclose standardised climate-related risk information in their filings with the SEC, but it was stayed as of April 2024. The acting chairman of the SEC also asked the court not to schedule oral arguments in the case for February 2026, effectively freezing the litigation. The earliest scope 1 and 2 emissions disclosures compliance deadline under the rule, in 2026 (for fiscal year 2025 reports), is still unknown, as to whether and how it will be enforced. A California lawmaker is pushing its own climate disclosure bills—SB 253 (Climate Corporate Accountability Act) and SB 261 (Climate-Related Financial Risks Act)—establishing a “patchwork” approach as the federal landscape leaves states to regulate. On March 17, the California Air Resources Board voted to pass the first rule of SB 200, setting the Scope 1 and Scope 2 emissions reporting due date for the first year as August 10, 2026.

This divergence between institutions is highly consequential. On the one hand, EU and Chinese jurisdictions are accelerating the implementation of mandatory climate disclosure regimes, shifting disclosure from a “voluntary choice” to a “legal obligation.” On the other side, a deadlock at the federal level in the U.S. and complementary activism at the state level have produced a distinctive pattern of “patchwork governance.”As Moody’s noted in its 2026 outlook, companies will have their “work cut out for them” in the coming year. They are contending with a chaotic array of rules derived from various jurisdictions, and, frankly, no one is quite sure what they need to do or when.

Carbon Pricing: The Big Shift from Rules to Reality

The highlight of the system application in March 2026 was certainly the formal entry of CBAM into its obligation period. So, following a two-year warm-up period, CBAM went live on 1 January. If you are importing products such as steel, cement, or hydrogen, you now need to account for all your carbon emissions. Just a heads-up: the actual bills for those carbon costs won't start hitting the books until 2027.

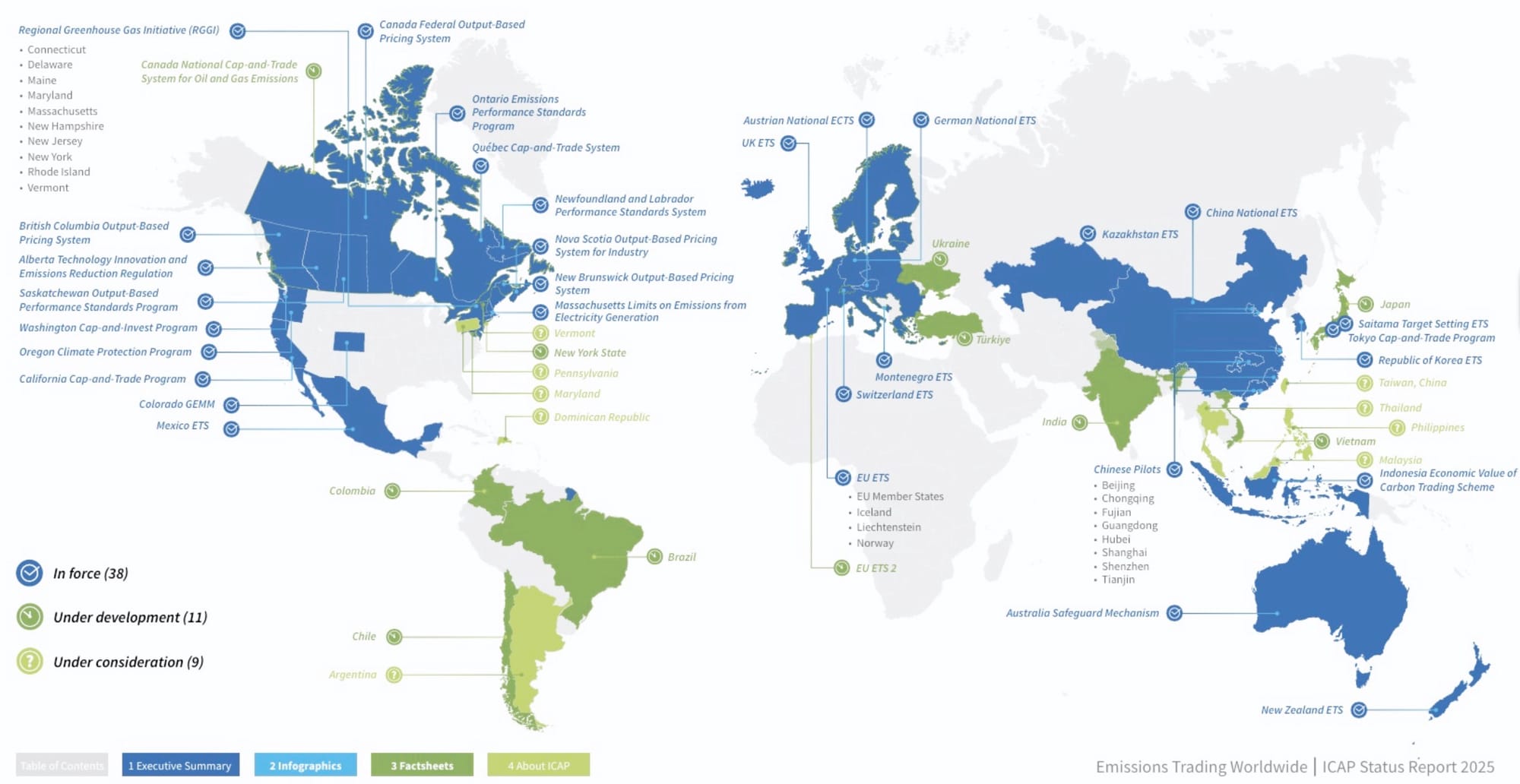

A key March deadline was March 31—the final deadline for importers to obtain CBAM-authorised declarant status. Pre-March 31 imports don't require approval. Post-March 31, though, you must have your formal authorisation in place before you import.As reflected in the most recent status report from the International Carbon Action Partnership (ICAP), the shift from “reality rules” is happening worldwide. Even though the EU’s CBAM establishes a direct financial link between international trade and carbon costs, it operates within a rapidly expanding global carbon market landscape. With 38 systems already in place and many more in the pipeline—including China’s national ETS and a range of regional programs across North America and Asia—the pressure to cut emissions from carbon-intensive industries is no longer limited to a few local jurisdictions. Instead, it’s increasingly becoming a standing condition for accessing global markets.Simply having an application in the system won't get you through customs anymore. Customs authorities in various countries have implemented online verification through the

; unauthorised entities will be unable to complete customs clearance.

In practice, the response from China's bulk commodity industries has been generally stable. According to Roland Berger's Global Senior Partner, the steel and aluminium industries initially covered by the CBAM have a high concentration, and leading companies have relatively mature compliance awareness and management systems. Their long-standing data collection and reporting practices help them better meet the carbon emissions reporting requirements for Scope I and Scope II. Coupled with years of preparation, steel and aluminium companies demonstrated a very high level of readiness when the CBAM officially came into effect.

However, deeper challenges are emerging. The EU has also proposed draft legislation to expand the scope of the CBAM to approximately 180 steel- and aluminium-intensive downstream products, including machinery and equipment, automobiles and their parts, and household appliances, starting in 2028 (See Appendix B for the full list of impacted products). If the scope is expanded to include downstream products and Scope III (complete carbon footprint) is included in future carbon-emission calculations, companies' compliance burden will increase significantly. Furthermore, the CBAM provides two carbon emission calculation paths—"actual emissions" and "default values." China’s Ministry of Commerce has just raised a problem with the EU’s carbon regulations. They say the "default values" applied to products from China are way too inflated. Given that those figures are set to increase annually until 2029, China is denouncing it as a discriminatory measure that handicaps its exporters.

Even more dramatically, during the formal imposition of the CBAM (Carbonised Currency Act), a debate was simultaneously unfolding over whether to suspend the mechanism. Due to soaring fertiliser costs caused by the Iran-Iraq War, the Irish government called on the European Commission to suspend carbon tariffs on imported fertilisers to reduce costs. However, the European Commission ultimately did not recommend suspending the CBAM, arguing that a suspension would make farmers more reliant on nutrients from outside the EU. This episode reveals the inherent tensions facing the CBAM—policymakers must balance ideal climate ambitions with realistic industrial competitiveness.

Meanwhile, the EU's institutional supply in sustainable finance is also accelerating. On March 18, the European Commission launched a public consultation on revisions to the EU classification standards, open until April 14, 2026, aiming to prepare for the upcoming amendments. On the same day, the European Court of Justice threw out a challenge to biomass energy. They essentially maintained their position and kept forest biomass on the 'sustainable' list. At the same time, the EU’s new ESG rating rules have been officially published and are expected to come into force as of July 2026.

Implementation Calibration: Tensions and Friction in Institutional Implementation

If institutional supply constitutes the main theme of the current ESG landscape, then the tensions and frictions in institutional implementation are an indispensable chord. We’re seeing these tensions pop up everywhere—from how countries work together on global rules to how companies handle day-to-day compliance, and even in how the courts are holding people accountable.

The Failure of Multilateral Climate Governance: The Collapse of COP30 and the EU's Diplomatic Shift

In March 2026, the COP30 talks entered their final sprint, only to end in a shocking deadlock. After nearly two weeks of negotiations, the draft text released by the host country, Brazil, made no mention of the words "fossil fuels" or "roadmap"—despite Brazilian President Lula's public support for the latter. More than 30 countries—including wealthy nations, emerging economies, and small island states—had previously jointly written to Brazil, stating that they would reject any agreement that did not include a plan to transition away from fossil fuels. More than 80 countries expressed disappointment at the end of the conference; these countries had originally pushed for the inclusion of a fossil fuel transition roadmap in the final agreement.

During the negotiations, EU Climate Commissioner Wopke Hoekstra warned, "What's on the table is unacceptable. Given how far we are from the goals we should be achieving, unfortunately, we really face a no-deal situation." Environment ministers from France, Germany, and other countries have rejected the draft agreement. French Minister for Ecological Transition Monique Barbout pointed out that oil-rich Russia and Saudi Arabia, as well as coal-producing India and "many" emerging countries, are obstructing the fossil fuel agreement.

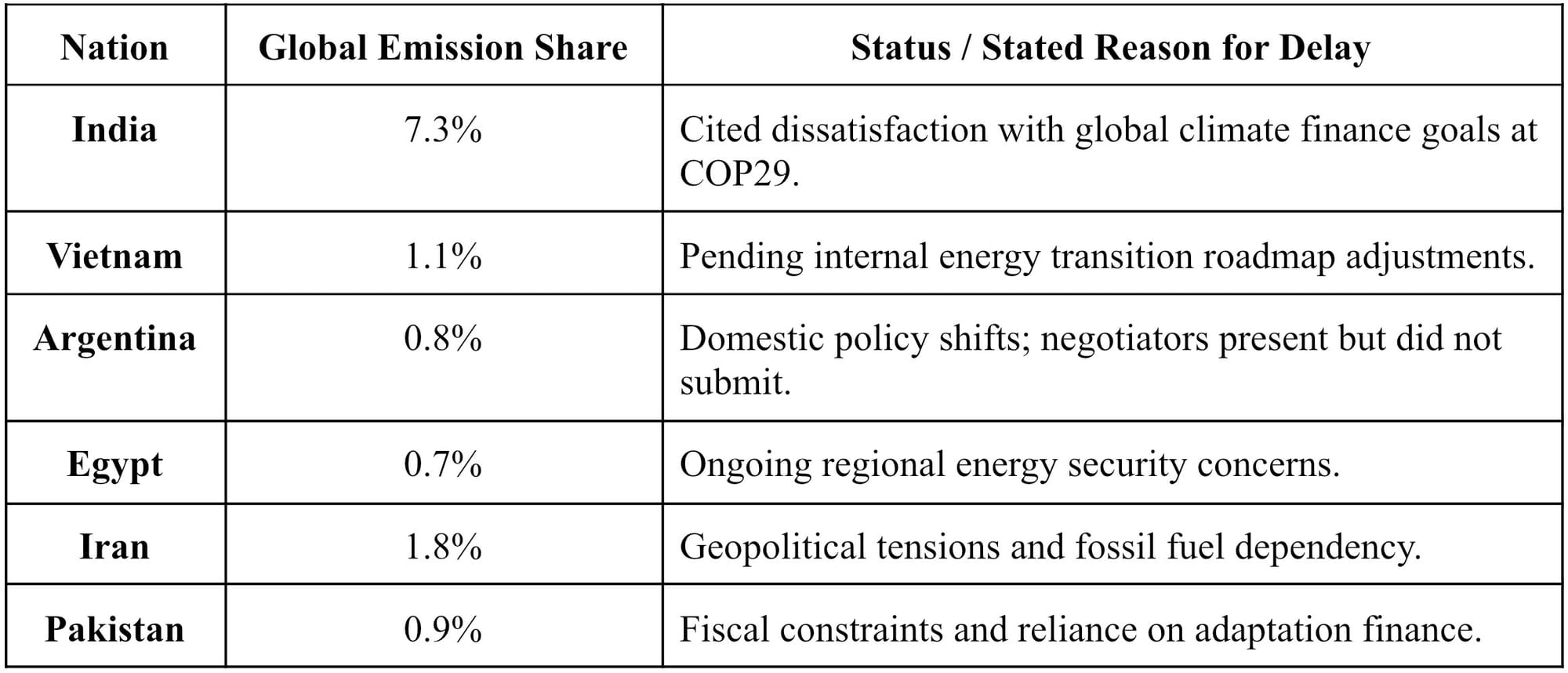

The breakdown of COP30 is not accidental, but a concentrated manifestation of the deep-seated failures of the multilateral climate governance mechanism. And yet a further concern remains that, as of March 2026, 62 countries have yet to submit revised versions of their NDCs (See Appendix E for the list of non-compliant nations)– with India, Vietnam, Argentina and Egypt among the large emitters on that list. These nations account for 22% of global greenhouse gas emissions. Over a year has elapsed since the COP30 deadline of 10 February 2025.

Therefore, the Paris Agreement Implementation and Compliance Committee met in Bonn from March 24 to 27 to discuss how to address countries that have not complied with their NDC submission obligations. However, the committee cannot punish countries; at most, it can only publicly condemn them and demand explanations.

With all these challenges piling up, the EU is stepping up its climate diplomacy. During the ministerial meeting on March 17, the focus was on leveraging Europe’s strengths—such as using science and 'leading by example'—to build stronger global alliances and make better use of the resources they’ve got.

France is pushing the EU to adopt a “stricter, more transactional” diplomatic approach, making fuller use of leverage such as trade agreements and official development assistance. An official from the French Ministry of Ecological Transition stated clearly: “We must better utilise the leverage at our disposal, especially our access to the single market, to promote what we define as Europeans – respect for the Paris Agreement.” Failure to submit to the NDC could result in the suspension of trade agreements.

This shift has profound implications. It marks a shift in the EU from a role as a “rule-maker”—that is, leading the world by setting an example—to a role as a “rule enforcer”—that is, using hard constraints, such as market access, to compel other countries to fulfil their climate commitments. This is a key signal of the transformation of global climate governance from “voluntary commitments” to “conditional constraints.”

The stark contrast between the proposed fossil fuel roadmap and the final hollowed-out text—as detailed in Appendix E—serves as the definitive proof of the breakdown in multilateral climate diplomacy.

Restructuring of Trade Rules: From Efficiency Competition to Rule Competition

The activation of the Carbon Border Mechanism (CBAM) represents a deep rewrite of the world trade rules. As the CBN analysis highlights, the rules of world trade are being transformed from competition based on efficiency to competition based on rules. Chinese companies must incorporate carbon costs into their core competitiveness and build carbon management systems to cope with supply chain reshaping and the new global green trade order.

In the short term, the compliance pressure on China's bulk commodity industries is generally manageable. However, in the long term, challenges are accumulating. First, the EU has proposed expanding the scope of the CBAM to approximately 180 downstream products, meaning that export companies in more industries will be included in the regulatory scope. Second, the EU released a legislative proposal for the Industrial Accelerator Act (IAA) in early March, striving to achieve "manufacturing reshoring." This series of new regulations, combined with the CBAM, forms a complex green trade barrier. Third, the EU also plans to impose comprehensive carbon footprint requirements on products such as machinery and equipment, automobiles and their parts, and household appliances. Scope three carbon emissions will become a new compliance challenge.

China has clearly expressed its concerns. The Ministry of Commerce pointed out that the EU's disregard for China's significant achievements in green and low-carbon development, setting a significantly high default value for the carbon emission intensity of Chinese products, and planning to expand this scope from 2028, constitutes a new form of trade protectionism. China stated that it will resolutely take all necessary measures to respond to any unfair trade restrictions. This trade friction surrounding carbon pricing will continue to escalate in the coming years.

Meanwhile, the US is also considering a similar carbon border adjustment mechanism. In the COP30 talks, the EU is facing strong resistance from a group led by China and India. They’re clearly opposed to the EU’s “carbon tariffs” on imports such as steel, aluminium, and fertilisers. At the same time, the UK and Canada are preparing to introduce their

own versions. What began with the EU acti on its own has now become a high-stakes competition, with major economies all working to reshape the rules of global trade.

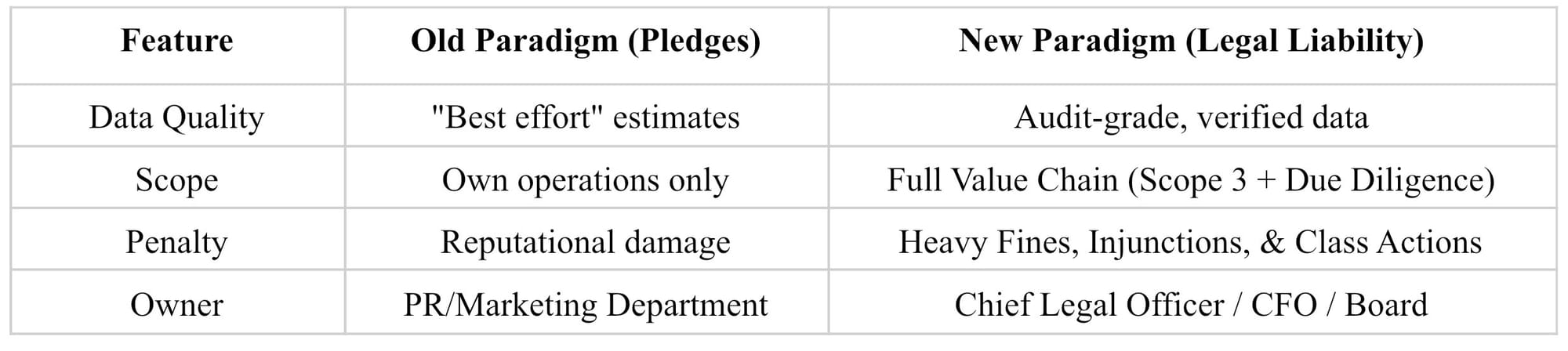

Upgrading Accountability Mechanisms: The Critical Point from "Soft Constraints" to "Hard Constraints"

Recently, a series of ESG-related lawsuits and settlements has revealed that corporate ESG accountability mechanisms are undergoing a profound shift from "soft constraints" to "hard constraints."

On March 2, Steve Marshall, the attorney general of Alabama, announced a $29.5 million settlement with Vanguard Group and its affiliates to resolve claims that the asset manager compromised investors' returns in the name of environmental pursuits. This case is one of several, including a multistate antitrust lawsuit filed in November 2024 by Texas against defendants BlackRock, State Street, and others. These states allege that the asset management firms leveraged both their assets under management and market influence to pressure coal companies to pursue ESG-aligned strategies, thereby creating a constrained supply of coal and spiking energy prices. As part of the settlement, Vanguard pledged not to use its shareholding to guide business strategy, threaten divestment to influence company decisions, or nominate directors or shareholders to advance ESG goals. It is noteworthy that Vanguard did not admit to any wrongdoing, and the settlement explicitly stated that it was to "avoid the burden and costs of litigation." However, the local court had previously dismissed motions to dismiss the other defendants, and the lawsuits against BlackRock and State Street will continue.(As detailed in Appendix D, these settlements have evolved from symbolic fines to restrictive legal covenants that fundamentally alter corporate governance.)

The significance of this case extends far beyond the settlement amount. It marks a shift in the retaliation against ESG investing from the political rhetoric level to the judicial enforcement level. Republican-led state attorneys general view ESG as an anti-competitive practice—coordinated action to limit fossil fuel supplies—rather than as well-intentioned environmental protection. This shift in characterisation will have a profound impact on ESG investment strategies in the global asset management industry. In fact, Vanguard is withdrawing from its climate initiative, effectively waiving its commitment to advancing climate goals through shareholder action as part of the settlement.

Almost simultaneously, Glencore faces serious greenwashing lawsuits in Australia. On 30 March 2026, the Wonnarua People Plains Clan and the Lock the Gate Alliance—representing Indigenous Australian communities—submitted a complaint to the Australian Competition and Consumer Commission (ACCC) and the Australian Securities and Investments Commission (ASIC), accusing Glencore of issuing misleading statements about its climate implications and the steps it has taken to recognise traditional landowners. Glencore operates 17 coal mines in Australia and is the country's largest coal producer and largest contributor to coal mine emissions. While Glencore publicly claims to have a decarbonization plan, legal investigations by the Office for Environmental Protection found no evidence to support these claims. In fact, Glencore is expanding its coal production, and its net-zero claims may constitute harmful greenwashing under the Corporations Act or the Australian Consumer Act. London-based ClientEarth supported the action, writing to the UK Financial Conduct Authority (FCA) and urging it to coordinate a strong response with ASIC.(As detailed in Appendix D, these settlements have evolved from symbolic fines to restrictive legal covenants that fundamentally alter corporate governance.)

This matter is exceptional as it is the first time that Indigenous rights, consumer protection, and climate information disclosure have been combined, presenting a novel ESG accountability concept—not at the level of environmental performance itself, but with respect to the accuracy of the disclosures and the respect for the rights of impacted communities. The Glencore case will be groundbreaking in international greenwash litigation.

Furthermore, in March 2026, Amazon Data Services reached a $20.5 million settlement regarding nitrate contamination of groundwater in Oregon. The Ontario Superior Court has certified a class-action lawsuit against Barrick Minerals, in which its shareholders accused it of making false and misleading statements about its compliance with environmental permits, its capital expenditure estimates, and the date of first gold production for its Pascualama mine project. DTE Energy appealed a $100 million federal court ruling concerning sulphur dioxide contamination at its Zug Island facility.

According to relevant data, as of March 2026, 74 listed companies in China had exposed 104 risk events, with a risk index of 161.65. Of these, governance risks accounted for 26.8%, environmental risks for 11.8%, and social risks for 61.4%. The issue of wage arrears affecting Jinke Real Estate Group nationwide, systemically and on a large scale, has become a centre of attention, impacting formal employees and migrant labourers, with the longest period of unpaid wages being 16 months. This case highlights the ironclad rule in the ESG framework that "governance determines survival"—corporate governance failures directly lead to the emergence of social risks, ultimately jeopardising the company's survival.

These regular litigations and settlements reveal a trend: ESG has shifted from the soft constraint category of "voluntary commitments" to the hard constraint categories of "mandatory disclosures" and "legal liabilities." Be it greenwashing allegations, anti-ESG antitrust lawsuits, or labour rights lawsuits, they all tell the same story: the courts are becoming a key arena for ESG governance. The legal risks associated with corporate ESG statements are rising sharply.

Market and Investment Divergence: A Reassessment of Capital Flows

Current capital market data reveals a highly divergent landscape in global ESG investment.

Moody's, in its 2026 outlook report, indicates that global sustainable bond issuance is projected to reach $900 billion in 2026, roughly flat compared to 2025. Investments addressing the climate mitigation and adaptation gap will continue to receive support, but political headwinds and other priorities will dampen issuance in some regions.

Environmental projects will continue to dominate the sustainable bond market, supplemented by investments in transformation, adaptation, and digital infrastructure. Moody's also specifically highlights the impact of AI on electricity demand—by 2030, data centre power consumption could exceed 2200 terawatt-hours, placing profound pressure on energy transition and grid infrastructure.

The regional distribution shows a clear "strong Europe, weak America" pattern in the ESG bond market. In the longer term, to 2026, global ESG bond supply will likely remain flat, and Europe will continue to dominate issuance momentum. US issuers are seeing weak overall intentions to issue, as they remain influenced by policy and market conditions – and it is expected that overall ESG bond activity will remain muted in 2026. This divergence resonates with the "anti-ESG" movement sweeping through the US domestic ESG investment market.

The US ESG fund market is undergoing a severe adjustment. According to Morningstar data, 91 US ESG funds closed in 2025, while only 9 new funds were launched. US ESG funds experienced net redemptions for the third consecutive year, totalling $21 billion. Investors pulled out $8.6 billion from global sustainable open-ended funds and ETFs in Q1 2026. The ESG Aware MSCI USA ETF (ESGU) was one of those with the largest outflows, losing $6.5 billion in March alone, 15 times the second-largest loss-making fund of the quarter, bringing its assets under management down to around $14.2 billion. Yet it’s worth noting that, despite ongoing fund closures and net outflows, US sustainable funds' total assets still increased from $344 billion at the end of 2024 to $368 billion at the end of 2025, indicating that existing asset appreciation somewhat offset capital outflows.

This disparate trend in ESG investing mirrors broader systemic contradictions. On the one hand, driven by energy security and affordability imperatives, sustainable in 2026, but the worry over the cost and insurability of climate risk is pressing. On the other hand, political polarisation has led to the high politicisation of ESG in the US, with the "anti-ESG" movement exerting substantial pressure on ESG investment through legislation and litigation.

Recommendations

Based on the above analysis, the following strategies are proposed for enterprises and investors.

Establishing Institutional Compliance Capabilities

Faced with an increasingly complex ESG regulatory environment, enterprises need to establish institutional compliance capabilities. At the cross-border compliance level, enterprises must establish a comprehensive management system covering carbon data accounting, certification, and disclosure. Taking CBAM as an example, enterprises not only need to meet current reporting requirements but also anticipate the compliance pressure after the scope expands to downstream products. Specifically, enterprises should establish a carbon emission data governance system covering the entire process from data collection and verification to reporting; cultivate internal carbon accounting capabilities to reduce excessive reliance on external third parties; pay attention to the difference between default values and actual emission values, and proactively strive to adopt the actual emission value path. Especially when facing excessively high default values set by the EU for Chinese products, enterprises should actively seek to reduce carbon costs through actual emission data.

At the level of information disclosure, Chinese enterprises are in a period of institutional transition from "voluntary disclosure" to "mandatory disclosure." A-share listed companies are required to disclose ESG information by April 30, 2026. Reporting timeliness is crucial for companies to ensure data quality, and by the end of March, data quality had already become a vital scoring factor in this first review. As demonstrated in the Shanghai Stock Exchange's case studies, high-quality ESG reports should reflect a dual substance: addressing both the financial impact of ESG issues and the impact of corporate activities on the external environment and society. Companies should avoid a disconnect between disclosure and operations, truly integrating ESG strategy into major decision-making and daily operations.

Building a Firewall Against Greenwashing Legal Risks

With cases such as Glencore's greenwashing lawsuit, the legal risks of corporate ESG statements have moved from theoretical possibilities to real threats. Companies need to create a three-level defense mechanism: first, all publicly disclosed ESG statements are based on verifiable data to form a traceability chain of “statement-data-evidence”, second, key statements such as decarbonization pathways and net-zero commitments should be subject to independent third-party audits or verification to mitigate the risk of “over- commitment”, and third, the company should establish a board-level assurance mechanism for the accuracy of ESG statements and integrate ESG information disclosure into the internal control system of the company. The CSRC (China Securities Regulatory Commission) has announced that information disclosure will be approved and controlled by the board of directors, further strengthening the board's legal responsibility for ESG disclosure.

Strategically Navigating a Fragmented Landscape

Faced with the fragmentation of global ESG regulation—the EU's aggressive approach, China's institutional development, and the regulatory stagnation and state-level intervention in the US—multinational corporations need to adopt differentiated strategies. Moody's 2026 outlook suggests that large multinational corporations, in particular, face the challenge of fragmented requirements and timelines across different jurisdictions. Companies need to develop a two-level structure of "compliance benchmark + regional adaptation": take the international benchmark, including the ISSB as the core standards, and make adaptations for regional markets, such as the EU, China, and California. From a technology standpoint, investment should primarily go into data infrastructure and carbon accounting systems, since these will provide lasting value for compliance, regardless of the regulatory regime. At the same time, companies should understand that carbon pricing tools like CBAM are changing the rules of global trade. As First Financial Daily points out, future competition will occur "between chains and between regions." Proactively building green supply chain capabilities is not only for compliance but also to gain a competitive edge in the race to the rules.

Focusing on Structural Opportunities in ESG Investment

For investors, the current differentiation in the ESG market presents structural opportunities. On the one hand, US ESG funds are experiencing outflows and political scrutiny, which could result in undervalued, high-quality targets; on the other hand, ESG bond issuance is still picking up pace in European and Asian markets, with strong allocation demand. Transformation, adaptation, and investments in digital infrastructure are expected to be key growth areas in the sustainable bond market, according to Moody's. Investors ought to be able to differentiate “ESG labels” from “real ESG performance,” and they should look for companies with well-defined transformation pathways, concrete actions to reduce emissions, and solid governance. As ESG becomes more advanced, even simple “green” labels are no longer sufficient to convince investors to go there. Instead, it is important to have a credible story, based on well-considered metrics, and with some path forward for investors, one they can get behind.

Conclusion

Ten years ago, a new chapter in multilateralism in climate governance was written. Ten years later, the chapter is written by reality and institutional tension. The crisis in the COP30 negotiations revealed that the multilateral climate governance mechanism was not sufficient; 62 countries failed to submit their NDCs by the deadline. The EU is shifting from “rule maker” to “law enforcer” by imposing hard limits, such as on market access, to drive global climate action.

The institutional environment for ESG is going from ”soft law” into “hard law“; CBAM embeds carbon costs into trade rules, China's ESG disclosure of A-shares puts sustainability information into legal responsibility; the lawsuit between Glencore and Vanguard shows that ESG statements can go from theory to reality for companies and investors. Regulation is growing, but institutional tensions increase. Institutional supply is growing; institutional tension is growing. This will be the core theme of global ESG going forward.

For policymakers, the challenge is to design viable, acceptable, and adaptive institutional policies while maintaining climate ambition. For businesses, the challenge is to develop strategic resilience and compliance in an environment where regulation is increasingly fragmented. The challenge for investors is finding genuine ESG value amid differentiation rather than label-based storytelling.

At a deeper level, the current ESG picture reveals that real-world institutional building is not in legislation but in practice. When rules go from paper to reality, when commitments are held accountable, and when ambition is tested, global ESG governance is about to enter its “stress test” phase. The outcome of this test will largely depend on humanity's success or failure in responding to the climate crisis in the next decade.

Further Reading

Global ESG Policy and Regulatory Framework (2024–2026)

Detailed Case Studies of ESG Litigation and Settlements (2025–2026)

The Vanguard Group Settlement (March 2, 2026)

Total Settlement: $29.5 Million.

Case Background: Allegations by the Alabama Attorney General that Vanguard prioritized ESG agendas over fiduciary duties to maximize financial returns.

Key "Hard Constraint" Commitments (Restrictive Covenants):

• Voting Neutrality: Vanguard pledged not to use its proxy voting power to influence companies to adopt specific environmental or social goals.

• Anti-Divestment Pledge: Promised not to threaten divestment from fossil fuel companies to compel changes in business strategy.

• Governance Restriction: Prohibited from nominating directors specifically to advance ESG mandates.

• Transparency: Required to issue public disclaimers that its ESG-labeled products may underperform traditional benchmarks.

Glencore "Greenwashing" & Human Rights Complaint (March 30, 2026)

Parties: Wonnarua People Plains Clan & Lock the Gate Alliance vs. Glencore PLC.

Legal Basis: Australian Consumer Law & Corporations Act (Section 1041H - Misleading or Deceptive Conduct).

Core Allegations (Excerpted):

• Misleading Net-Zero Pathways: Alleged that Glencore’s "Climate Report 2024" failed to account for planned coal mine expansions (17 active mines in Australia), rendering its 2050 Net-Zero claim factually impossible.

• Misrepresentation of Indigenous Consultation: The Wonnarua people claim Glencore publicly stated it had "broad community support," while actively bypassing the Traditional Owners' opposition to the Hunter Valley coal projects.

• Scope 3 Omission: Failure to adequately disclose downstream emissions from coal exports, which constitute over 90% of Glencore’s total climate impact.

Barrick Gold Class-Action Certification (Ontario Superior Court)

Primary Allegation: Misleading shareholders regarding environmental compliance at the Pascua-Lama mine.

Legal Significance: The court certified that "environmental compliance statements" are material to stock price, meaning poor ESG performance now leads directly to Securities Fraud litigation.

COP30 Stalemate and NDC Non-Compliance Analysis

Key Emitting Nations Missing NDC Submission Deadlines (March 2026)

While 62 countries have failed to submit their revised Nationally Determined Contributions (NDCs) as required by the 2025/26 cycle, the following major emitters account for the bulk of the 22% global emission gap mentioned in Section 3:

Textual Comparison: The "Fossil Fuel Phase-Out" Controversy at COP30

The following table contrasts the ambitious "Roadmap" language supported by over 80 countries (including the EU and Small Island States) versus the final "Mutirão" draft released by the Brazilian presidency, which led to the stalemate.

Multilateral Governance Failure Metric

• Participation vs. Compliance: While 195 parties participated in COP30, only ~30% of parties have submitted 2035 targets that are fully aligned with a 1.5°C pathway.

• The "Finance-Ambition" Deadlock: Developing nations (led by India) have officially linked NDC ambition to the delivery of the $1 Trillion+ New Collective Quantified Goal (NCQG) on climate finance.

Key Metrics Summary from ICAP Status Report 2025

This appendix provides the quantitative data underlying the "Emissions Trading Worldwide" map featured in Section 2.3, highlighting the scale and economic impact of global carbon markets as of March 2026.

Global Emission Coverage and Market Scale

• Total Emissions Covered: Approximately 18.5% of global greenhouse gas (GHG) emissions are now regulated under an active Emissions Trading System (ETS).

• System Proliferation: * 38 systems in force (including the EU ETS, China National ETS, and various North American regional programs).

• 14 systems under development, primarily in emerging economies (e.g., Brazil, Indonesia, Turkey).

• 9 systems under consideration, indicating a continued expansion of carbon pricing as a standard policy tool.

Economic and Financial Impact

• Cumulative Revenue: Since their inception, global carbon markets have raised over USD 235 Billion in auction revenues.

• Revenue Allocation: In 2025 alone, over 70% of auction proceeds were reinvested into climate-related projects, including renewable energy R&D, industrial decarbonization, and social compensation for energy transition (e.g., the EU’s Social Climate Fund).

• Market Liquidity: Trading volumes in the EU ETS and the newly expanded China National ETS reached record highs in Q1 2026, signaling increased participation from financial intermediaries.

Carbon Price Convergence & Divergence (Critical for CBAM Analysis)

• The "Price Gap": * EU ETS: Averaging €85–€95/tonne in early 2026.

• China National ETS: Hovering around ¥90–¥110/tonne (~€12–€14).

• Strategic Implication: This significant price differential remains the primary justification for the EU’s CBAM. As EU free allowances are phased out, the "effective carbon cost" for exporters to the EU will converge toward the EU price level, as detailed in Section 2.3 of this paper.

Sectoral Reach (2025 Update)

• Power & Industry: 100% coverage in most active systems.

• Buildings & Transport: Now partially covered under the EU ETS 2 and various sub-national systems in North America.

• Aviation & Maritime: Full integration into the EU ETS as of 2025, with maritime reporting now a core compliance requirement for global shipping routes.

References

- Founder Securities Research Institute: The 15th Five-Year Plan sets the tone for the start of the year, with a target of reducing carbon emission intensity by 3.8% in 2026 [R]. 2026-03-08.

- Huachuang Securities: The EU officially establishes the world's first permanent carbon removal standard [R]. 2026-03-10.

- Pierag. ESG Perspective – March 2026 Edition [R]. 2026-03-09.

- Sustainable Development Economics Guide | 2026.03.04-03.11 [EB/OL]. 2026-03-19.

- Changjiang Securities. EU "Carbon Tariff" for the Environmental Protection Industry: How Will It Affect the Official Entry into the Fee Collection Period in 2026? [R]. 2026-03-15.

- First Financial Daily. EU "Made in China" New Regulations Frequently Appear, How Can Chinese Enterprises Break Through? [EB/OL]. 2026-04-08.

- Trade Enterprises. Practical Guide for Enterprises During the EU Carbon Tariff (CBAM) Collection Period [EB/OL]. 2026-03-26.

- Moody’s. Moody’s sets out its 2026 Outlooks: sustainable debt resilience and rising ESG-driven credit risks [R]. 2026-03-03.

- Clark Hill. ESG & Sustainability In 2026: Twists, Turns, And Trends [EB/OL]. 2026-03-23.

- PineBridge Investments. Insights into ESG Spring 2026 [R]. 2026-03-16.

- 21st Century Business Herald. A Must-Read for A-Shares! 56 Cases from the Shanghai Stock Exchange Set an Example for ESG Disclosure [EB/OL]. 2026-03-28.

- China Securities Journal. The First Test of Mandatory ESG Disclosure for A-Shares is Underway, with Data Quality Becoming an Important "Scoring Point" [EB/OL]. 2026-03-30.

- China Economic Net. Policy Efforts Drive ESG Management of A-Share Listed Companies into the "Fast Lane" [EB/OL]. 2026-03-06.

- Hart Center, East China University of Science and Technology. The Three Major Stock Exchanges Solidify the Foundation for Sustainable Development Disclosure, and the ESG "1531 Framework" Empowers High-Quality Development of Listed Companies [EB/OL]. 2026-03-04.